Asia Bitcoin company, Bitplanet, is trying to convert its Bitcoin treasury from a balance-sheet position into a source of mined BTC revenue.

The South Korean company said in a June 24 release that it signed a strategic memorandum of understanding with Nasdaq-listed Antalpha and mining ecosystem partners.

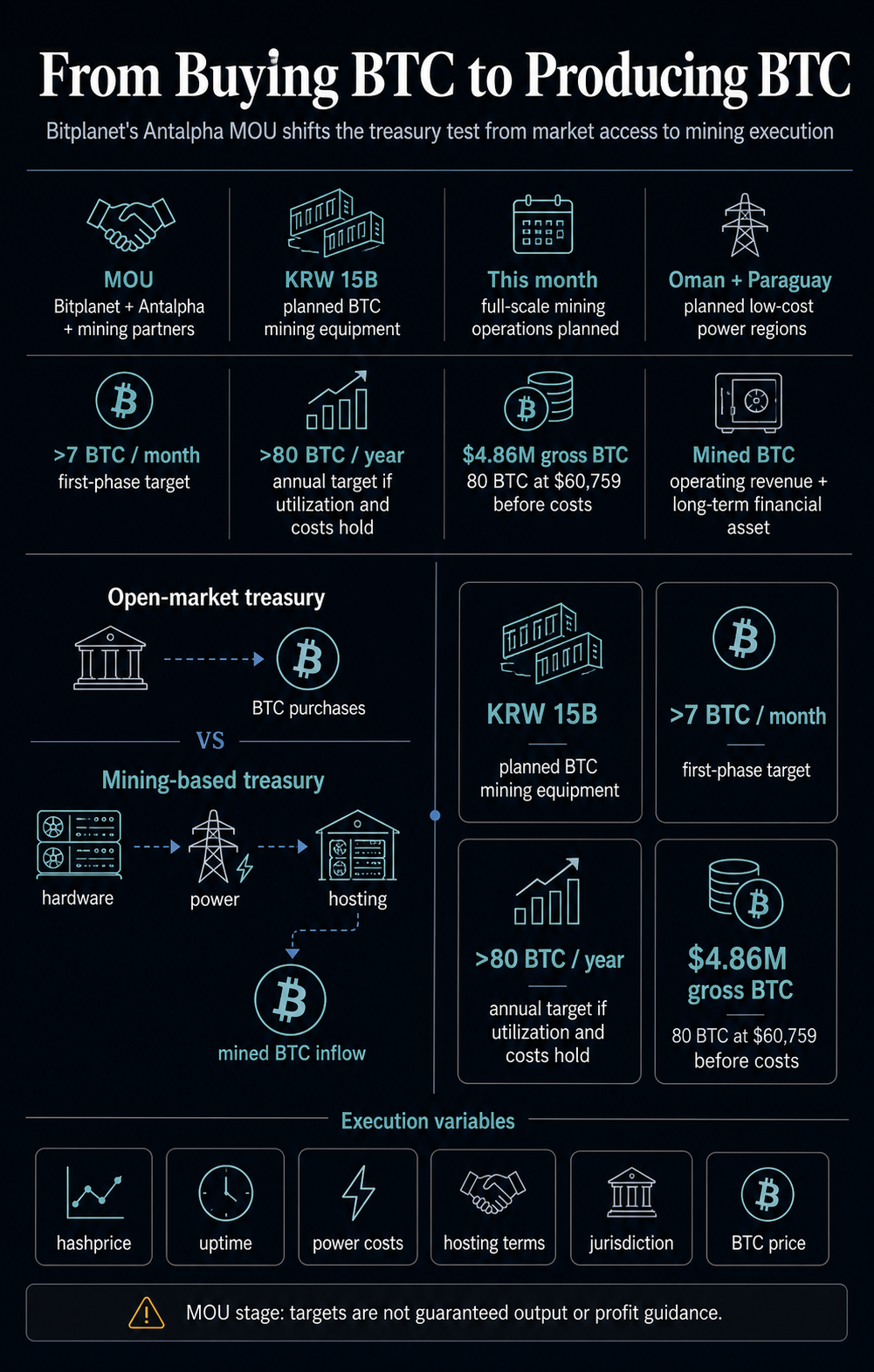

Under the MOU, Bitplanet plans to introduce KRW 15 billion in BTC mining equipment and begin full-scale mining operations this month.

The change pushes Bitplanet beyond the familiar corporate treasury playbook of raising capital, buying BTC, and letting the balance sheet carry the exposure.

A mining-based treasury is exposed to a different operating stack: hashrate, hosting contracts, power prices, equipment uptime, local execution, and whether mined coins are retained, sold, or pledged as collateral.

Bitplanet is presenting that second model as the next step for its corporate Bitcoin strategy. The company said mined BTC will be recognized as operating revenue and managed as a long-term financial asset across liquidity reserves, risk-hedging funds, and reinvestment capital.

Treasury Strategy Turns Operational

Bitplanet’s announcement extends the company’s earlier treasury accumulation. CryptoSlate previously covered Bitplanet’s SGA acquisition and its ambition to become one of the largest corporate Bitcoin holders, then later covered its daily Bitcoin accumulation push.

That earlier model was familiar: raise capital, buy BTC, and let the balance sheet reflect Bitcoin exposure.

The Antalpha deal points at a different question. Can a treasury company build a recurring Bitcoin production loop, where hardware, low-cost power, and hosting infrastructure feed coins into the balance sheet over time?

Bitplanet said the first-phase equipment is expected to target more than 7 BTC per month and over 80 BTC annually, subject to equipment utilization and power costs.

Using a Bitcoin price near $61,000, 80 BTC would represent about $4.9 million of gross BTC output before electricity, hosting, financing, repairs, taxes, and corporate overhead.

That math gives investors a scale marker rather than profit guidance. It also leaves open the question of whether the company can retain the mined BTC, reinvest it, or use it as collateral without weakening its broader treasury thesis.

| Model | What Adds BTC | Main Dependency | Key Risk |

|---|---|---|---|

| Open-market treasury accumulation | Purchases funded by cash, equity, debt, or other financing | Capital-market access and BTC price | Dilution, debt cost, or forced pauses in buying |

| Mining-based BTC inflow | ASIC equipment, hosting, power, and operating execution | Hashprice, uptime, power terms, and deployment quality | Mining margin compression or lower coin retention |

Antalpha brings more than a name to the announcement. The company priced its IPO in May 2025 and trades on Nasdaq under ANTA.

Its public materials describe a business built around Bitcoin mining finance, including mining-machine loans, hashrate loans, supply-chain credit, and margin-lending services through Antalpha Prime.

Antalpha’s IPO prospectus described lending products tied to rigs, hosting, maintenance, and mining operating expenses. Its Antalpha Prime materials add the operating link, describing financing arrangements in which mined BTC can be used as collateral for hosting, repair, and other service costs.

That creates the operating challenge for Bitplanet because mining is capital-intensive before it produces anything. Equipment has to be purchased or financed, shipped, installed, hosted, powered, maintained, and pointed at the network.

When a treasury company announces a target in BTC terms, the real test is whether the operating stack can produce coins at a cost below the value Bitplanet assigns to holding them.

Antalpha’s own results add a constraint to that story. The company reported a first-quarter 2026 total value of loans facilitated down 3% year over year and supply-chain TVL down 25%, even as revenue rose 52%.

That makes the Bitplanet MOU a test of execution inside a lending market that still has softer pockets.

Planned Power Markets Carry The Risk

Bitplanet said equipment is expected to be deployed in overseas regions with competitive electricity costs and stable power environments, including Oman and Paraguay.

It also described an overseas colocation model that combines outsourced operations and joint ventures.

That structure is central to the thesis and the risk. Mining margins can be won or lost on power terms, curtailment risk, hosting reliability, repair turnaround, and the share of mined BTC that leaves the company to cover costs.

A deployment in a low-cost power market can make sense on paper, but only if the contracts, uptime, customs, taxes, and counterparties hold up in practice.

The current mining backdrop makes that scrutiny necessary. Hashrate Index recently showed Bitcoin hashprice around $30.72 per PH per day.

In its May 2026 lookback, it noted hashprice averaged $36.60 and faded to $33.58 by month-end as difficulty rose.

VanEck’s mid-June Bitcoin ChainCheck estimated May 2026 miner revenue at about $1.12 billion, down 26% year over year, and noted that miners were selling BTC and moving into AI and high-performance computing.

Bitplanet is entering mining at a time when public-market investors are already differentiating among companies that own BTC, companies that can produce BTC, and companies that can convert power infrastructure into another revenue stream.

CryptoSlate’s recent coverage of miner AI infrastructure shows how quickly the market can reprice power assets before the operating buildout is complete.

Mining, therefore, changes what investors have to measure. The question shifts from how much BTC Bitplanet can buy to whether it can operate, finance, and retain the BTC it mines through a full cost cycle.

Those variables make Bitplanet’s next disclosures more important than the headline production target, since the economics will be set by contracts, machine performance, and coin retention after costs.

The Investor Test Is Coin Retention

The timing also lands during a more stressful phase for Bitcoin treasury companies.

CryptoSlate recently analyzed how Strategy’s STRC pressure can force tradeoffs between cash, BTC purchases, and dilution.

The same broad tension applies across the sector: a treasury strategy that relies primarily on external capital becomes harder to scale as financing terms worsen.

Mining offers a possible answer with clear tradeoffs. If Bitplanet can mine BTC at an attractive cost and retain enough of it, the company could supplement purchases with organic coin production.

If hashprice weakens, power costs rise, uptime disappoints, or hosting terms absorb too much output, the same mining program could become another capital-intensive burden.

The comparison with operating miners is also sobering. CryptoSlate recently reported that Bitdeer mined 921 BTC in May, while the market was still assessing how much of that production translated into a stronger retained treasury.

Bitplanet’s target of over 80 BTC annually is much smaller, but the same question applies: mined coins only improve a treasury model if enough of the value survives the costs of operations and balance-sheet demands.

South Korea’s corporate crypto backdrop adds one more layer. The Financial Services Commission said in 2025 that corporate virtual-asset transactions had been restricted in principle since 2017 and were being reopened in stages.

Bitplanet is therefore testing how a Korean-listed company can connect its Bitcoin treasury strategy, operating revenue, and overseas infrastructure without turning the model into a simple BTC-buying proxy.

The next signal is evidence of deployment: signed hosting or joint-venture terms, equipment hashrate, power-cost disclosures, monthly BTC production, and the amount of mined BTC remaining on Bitplanet’s balance sheet after expenses.

The post Bitplanet’s Antalpha mining deal tests whether Bitcoin treasuries can grow without constant buying appeared first on CryptoSlate.

The MOU points to mined-BTC revenue, but the real test is power cost, uptime, and coin retention.

The post Bitplanet’s Antalpha mining deal tests whether Bitcoin treasuries can grow without constant buying appeared first on CryptoSlate. Analysis, Digital Asset Treasuries, Featured, Investments, Mining, Bitcoin, Bitdeer, mining, Sora Ventures, Strategy

This articles is written by : Nermeen Nabil Khear Abdelmalak

All rights reserved to : USAGOLDMIES . www.usagoldmines.com

You can Enjoy surfing our website categories and read more content in many fields you may like .

Why USAGoldMines ?

USAGoldMines is a comprehensive website offering the latest in financial, crypto, and technical news. With specialized sections for each category, it provides readers with up-to-date market insights, investment trends, and technological advancements, making it a valuable resource for investors and enthusiasts in the fast-paced financial world.